Why Healthcare Sharing Ministry Costs Keep Rising

Rapid Cost Increases Should Concern Families and Ministries Alike

Many families are concerned with upcoming increases in their healthcare sharing ministry (“HCSM”) monthly share pricing – this year many HCSMs will nearly double their monthly shares from just a few years ago! These seemingly unpredictable increases have led many to wonder if there is an end in sight. But these shock increases are in fact predictable, based on well-established actuarial principles, and would typically be far less dramatic in a traditional health insurance environment. The trifecta behind these increases is comprised of 1) stabilizing HCSM growth, 2) no HCSM risk-assumption, and 3) pre-existing conditions exclusion, each of which we explain in this post.

Growth

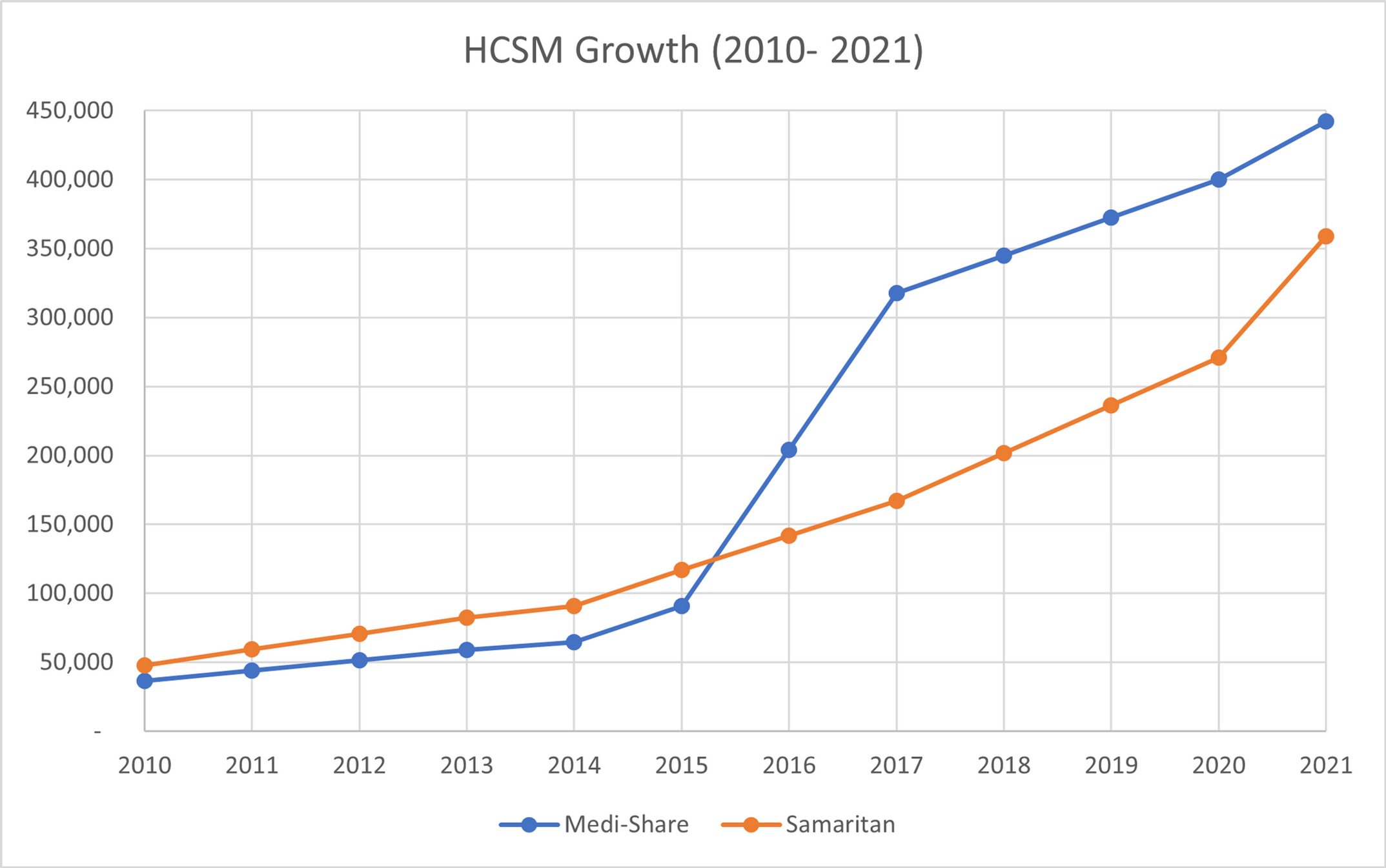

To understand HCSM’s growth pattern, it is important to consider their history. HCSMs exploded in popularity in the wake of the Affordable Care Act (“ACA”). HCSMs provided an avenue of escape from the ACA’s double-whammy of increased premium rates and mandated coverage.((Premiums rose 121% for the first five years of the ACA (Rate Review Data (cms.gov)); coverage was mandated per § 500A of Pub. Law 111-148 (11th Congress) )) The exponential growth trend continued for several years as displayed in Figure 1, which charts the enrollment of two major HCSMs from 2010 to 2021.

Figure 1 1

But recent enrollment seems to be stabilizing. For example, Medi-Share self-reported enrollment dropped 4% from 2021 to 2022 – new enrollment comprised 20.2% of overall enrollment in 2021, but just 10.7% in 2022.2 While the market for Christian values-aligned products remains largely untapped, this narrower market – i.e. families willing to stomach the inherent risk that comes with HCSMs – may be saturated. Additional headwinds to enrollment growth in 2022 and 2023 include the temporary increase in federal subsidies to purchase on-exchange ACA plans, improving the affordability of ACA coverage for some Americans. This stabilizing growth pattern is the first key to understanding pricing increases.

No Risk Assumption

HCSMs do not assume risk – here, it is important to understand what HCSMs are (and are not). HCSMs are unlicensed, largely unregulated organizations that facilitate payment for participants’ healthcare costs, usually through monthly “sharing” costs. Typically, participants submit their medical bills to the HCSM, and the HCSM matches participants who have medical bills with other participants to facilitate bill payment. HCSMs are sometimes viewed as a health insurance alternative. But unlike insurers, HCSMS 1) have no legal obligation to pay medical bills, 2) are not subject to insurance regulator oversight, and 3) do not assume risk.((There is a lot to unpack in differentiating HCSMs from insurers, which is important in its own right and will be the subject of a future blog post. )) This third feature means HCSMs typically do not accumulate reserves for future changes in needs. In the HCSM world, “perfect” pricing means matching annual revenues (i.e., participants’ monthly share contributions) with annual expenses (i.e., medical and administrative expenses) – without generating reserves necessary for future unexpected medical costs. Setting the monthly share price without accounting for reserves accumulation is the second key to understanding pricing increases.

Pre-Existing Conditions Exclusion

HCSMs typically exclude pre-existing conditions, which means certain illnesses and conditions are not eligible for “sharing” in the first year or so. This makes the initial risk pool very healthy, and the associated medical costs of first-year enrollees remain artificially low. But as participants stick with the product, they eventually develop new illnesses and conditions that incur expenses that start to add up. For so long as the HCSM is enrolling new participants each year, the new enrollees’ low and predictable healthcare costs can offset the relatively higher costs of second, third, and fourth-year participants. The exponential growth pattern prior to 2022 allowed HCSMs to keep monthly sharing costs very affordable.

But as new enrollment stabilizes, the risk pool normalizes to reflect actual lifetime illnesses and associated medical expenses. Reality sets in, and HCSMs must increase monthly sharing costs to keep up with growing claims submissions.

Perfect Storm and Death Spiral

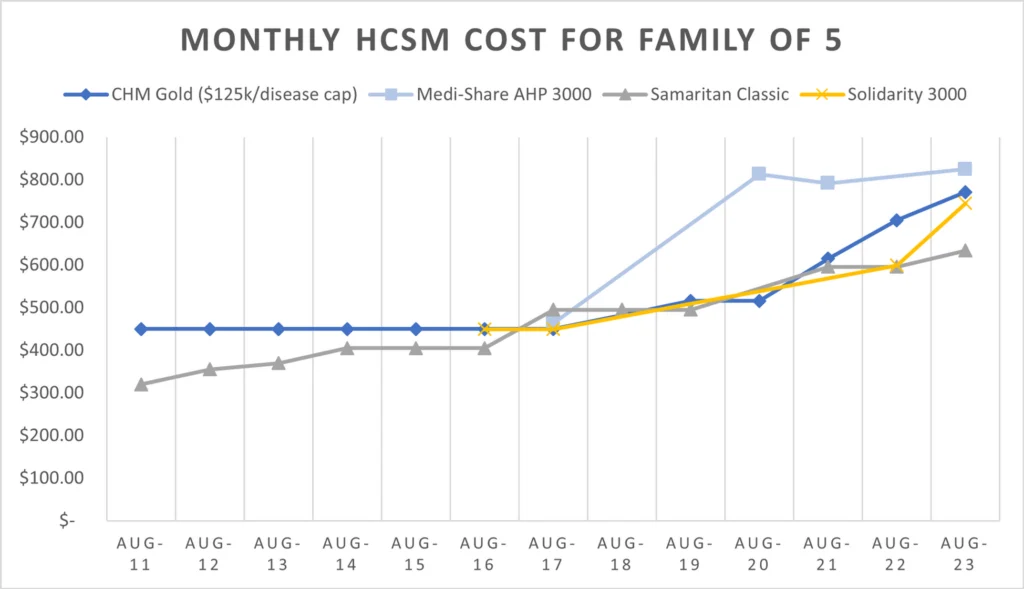

This explains why healthcare sharing ministry costs keep rising. HCSMs were initially extremely affordable – in 2017, a family of 5 could purchase a HCSM product for roughly $400 per month. More recently, those monthly costs have nearly doubled across the major HCSMs (see Figure 2).

Figure 2 3

These increases are a predictable effect of the volatile combination of 1) lack of policy reserves and 2) pre-existing conditions exclusion. These two features can only co-exist in equilibrium when a third element – enrollment growth – is strong. When enrollment growth stabilizes, imbalance ensues, and price increases are inevitable to keep up with increasing medical expenses.

Worse yet, the inevitable price increases can result in a “death spiral”. In this scenario, large premium increases further depress new enrollment and cause healthy participants to drop their coverage, leading to an even unhealthier risk pool, which in turn leads to further price increases.

How Insurers Avoid Death Spirals

To be sure, health insurers increase premiums for a variety of reasons, including inflation, medical costs, and changes in coverage or health status. But insurance premium pricing increases tend to be more predictable and stable compared to the HCSM world. This is because insurance companies assume risk, and therefore calculate lifetime expected costs as part of the underwriting process that determines policy premiums. In other words, insurance companies predict that new members will eventually become sick, and price for it up front. This results in a “smoothing out” of premium prices that are largely immune from stagnating enrollment growth.

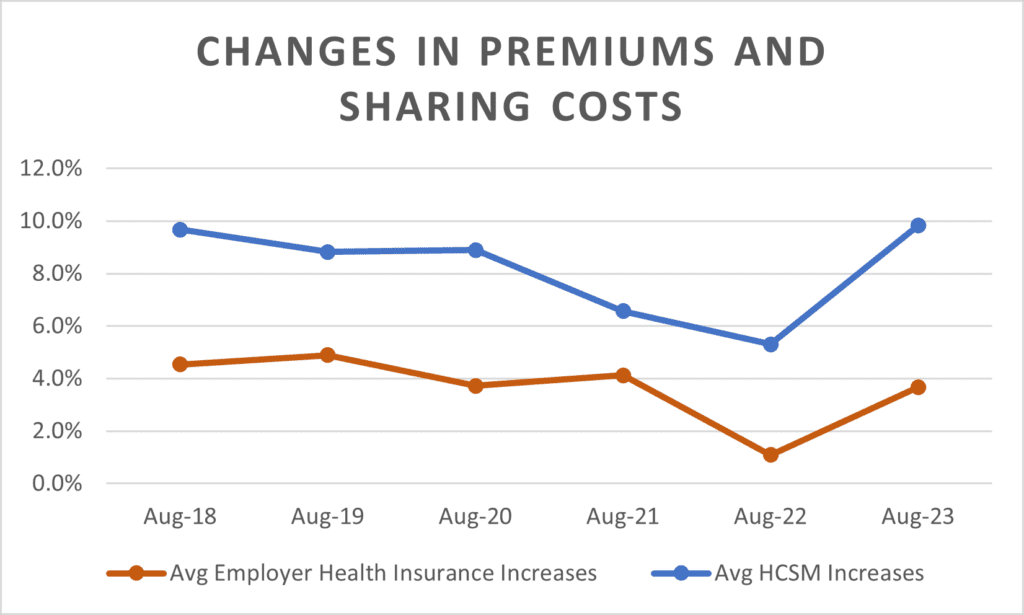

Figure 3 shows that the average year-to-year rate changes for HCSMs have consistently outpaced (and often doubled!) that of employer sponsored health insurance. While not a perfect proxy for off-exchange individual marketplace products, pricing actuaries in both insurance markets are trained to maintain stable premium increases through adequate reserving and pricing calculations. This allows for significantly more stability in health insurance pricing compared to HCSMs – this is part of the stability families seek when shopping for health insurance.

Figure 34

Conclusion

Rigorous actuarial pricing and regulatory oversight are unique features of the insurance industry that protect consumers from unexpected pricing increases and death spirals. This is just one of the many reasons we believe Christians need a faith-based insurance alternative to HCSMs and are launching Presidio to serve as the financially secure option families deserve.

- Author’s calculations based on Health Care Sharing Plans and Arrangements in Colorado (Colorado Department of Regulatory Agencies Division of Insurance) (hereinafter, the “Colorado Report”); The State of the Ministry, 2017 (Samaritan Ministries); and Health Care Sharing Ministries: an Uncommon Bond (Charlotte Lozier Institute). Note that enrollment numbers in this unregulated industry are notoriously difficult to ascertain. More consistent data is anticipated October 2023, when the Colorado Department of Regulatory Agencies Division of Insurance publishes its 2022 report. For purposes of the Colorado Report “Medi-Share” is reported as Christian Care Ministries dba Medi-Share and may be broader than just the Medi-Share product offered by Christian Care Ministries. [↩]

- See 2022 Annual Report (Christian Care Ministry) and 2021 Annual Report (Christian Care Ministry) archived from the original. Again we note that HCSM enrollment numbers are difficult to ascertain, and Christian Care Ministry’s self-reported annual numbers differ from the numbers reported to the Colorado Department of Regulatory Agencies Division of Insurance (neither report details, e.g., exact time period, how members are calculated, or which products are included or excluded). Nonetheless, Christian Care Ministries’ annual reports note decreases in total members (356,352 as of 6/30/22, down from 369,500 as of 6/30/21) and total new members (34,455 in 2022, down from 74,747 in 2021). [↩]

- Monthly costs for average family of 5 using historic advertised costs of highest tier plan without add-ons or additional protections. All 2023 prices are based on respective HCSM websites as of August 25, 2023. Medi-Share historic pricing is based on historic MedishareReviews.com archives accessed through http://web.archive.org/. All other historic pricing was derived from the respective HCSM’s historic websites using archived websites accessed through http://web.archive.org/. Medi-Share pricing could not be located prior to 2017. Note that Solidarity launched in 2016. [↩]

- See footnote 5. 2023 employer health insurance change represents author’s estimate based on 5-year trend. 2022 employer health insurance data from Employer Health Benefits 2022 Summary of Findings (KFF). All other employer health insurance data adapted from 2021 Employer Health Benefits Survey (KFF). [↩]